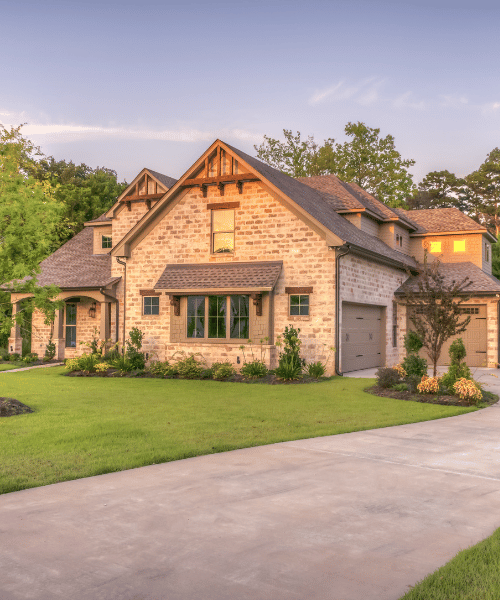

Getting ready for a real estate appraisal in Northwest Indiana? Don’t let the paperwork scare you. 219NWI Appraisal Group works all over Lake, Porter, and LaPorte counties, and we know exactly what you need to have ready. The whole process is pretty straightforward once you understand what the appraiser is looking for.

What Does an Appraiser Actually Do?

Here is what happens when the appraiser shows up at your door. They will spend about thirty to sixty minutes walking through your home. They measure every room, check the roof, test the heating and cooling, and look at the overall condition. They count rooms and windows and take plenty of pictures. Then they go back to the office and compare your house to similar homes that have sold nearby. That is how they come up with the number. The lender needs this number to make sure they are not lending more money than the house is worth. Pretty simple, right?

The Paperwork You Absolutely Need

Let’s talk about the documents. Having these ready makes everything move so much faster.

Proof that you own the place: You need your property deed. This shows who owns the house and exactly where it sits. Keep this in a safe place and have it ready. You also need your driver’s license or passport so the appraiser knows you are really the owner.

Your property tax records: Grab your latest tax receipt or the county assessment. This shows what the county thinks your home is worth. 219NWI Appraisal Group looks at these numbers all the time in Lake, Porter, and LaPorte counties. It gives the appraiser a good starting point.

Your floor plans if you have them: If you have the original plans from when the house was built, show them to the appraiser. They show the layout and room sizes without anyone having to guess. Did you finish the basement? Add a new deck? Remodel the bathroom? Bring those permits too. It proves the work was done the right way.

Your purchase agreement: If you still have the contract from when you bought the house, include it. This tells the appraiser what you paid and helps them see how values have changed over time.

Your encumbrance certificate: This sounds complicated but it is really just a paper that says nobody has a claim against your property. No liens, no legal issues. Lenders need to see this before they approve your loan.

Your HOA paperwork: If your neighborhood has a homeowners association, give the appraiser the rules and the current dues. They need to understand what extra fees or restrictions come with the property.

Records That Show How You Take Care of Your Home

Maintenance receipts are gold. Keep every receipt for big repairs. New roof? New furnace? New water heater? Show them. These receipts prove you have taken good care of your house. And homes that get good care almost always appraise higher.

Home inspection reports help too. If you had a home inspection recently, hand that over. It covers the electrical system, plumbing, foundation, and structure. The appraiser is not doing a full inspection, but this information helps them understand the property better.

Insurance records tell the story. Your homeowner’s insurance papers show any claims you have made and what repairs happened afterward. This gives the appraiser the full picture of your property’s history.

A Few Tips to Make Things Go Smoothly

Make sure the appraiser can get everywhere. That means the attic, basement, and crawl spaces. Move boxes and furniture that block the way. Clear paths through every room.

Broken windows? Fix them. Peeling paint? Scrape and repaint. Water pooling near the foundation? Fix the drainage. These small things can cause big problems if you ignore them.

Appraisers focus on three things. Location comes first, hands down. The condition of your home is second. Legal issues like liens come third. Amenities like parking and security features also matter, depending on what buyers in your area expect.

What If You Are Missing Some Papers?

Do not stress if you cannot find everything. 219NWI Appraisal Group can work with whatever you have. Just be honest about what is missing. You can usually get copies from the county records or your mortgage company. Call the team if you need help figuring it out.

You don’t always need someone to tell you it’s time for a Commercial Property Appraisal. Sometimes, the signs are already there, you just don’t realize it. Have you been thinking about selling your property?

Or maybe buying another one? Perhaps you’re planning to refinance, or you’ve recently spent money making improvements. If any of that sounds familiar, this is a good time to stop and ask yourself one simple question.

“Do I actually know what my property is worth today?”

Not what it was worth five years ago.

Not what a neighbor thinks it’s worth.

Not what an online estimate says.

What it’s worth today. That’s exactly what a Commercial Property Appraisal helps you understand.

Have you been saying, “I’ll deal with it later?”

A lot of property owners do. Life gets busy. The property is doing well. Nothing feels urgent. So, the appraisal gets pushed to the bottom of the list. But here’s the thing. When you finally need an appraisal, you usually need it quickly.

Maybe you’re about to sell. Maybe the bank needs one. Maybe you’re making an important business decision. Getting ahead of it gives you one less thing to worry about.

Are you thinking about selling?

If selling has been on your mind, don’t wait until the “For Sale” sign goes up. Start by finding out what your property is worth. That’s one of the hardest questions every seller has. “What should I ask for my property?”

Ask too much, and buyers may walk away. Ask too little, and you could leave money on the table. A Commercial Property Appraisal helps you start with real market information instead of guessing.

Are you getting ready to buy?

Buying commercial property is exciting. But it’s also a big financial decision. Before you spend that kind of money, wouldn’t you want to know if the asking price is fair? Most people would.

That’s another reason a Commercial Property Appraisal is so valuable. It helps you understand what the property is really worth before you commit.

Have you made improvements recently?

Think about everything you’ve done over the last few years. Did you replace the roof? Update the offices? Repave the parking lot? Improve the building?

If you’ve invested money into your property, you’re probably wondering if those improvements have added value. A Commercial Property Appraisal helps answer that question.

Instead of wondering… You’ll know.

Has it been years since your last appraisal?

Here’s a simple question. When was the last time your property was appraised? If you have to stop and think about it… It’s probably been a while. Commercial real estate changes all the time.

Property values change.

Neighborhoods change.

The market changes.

Your property’s value may have changed too.

Getting an updated appraisal helps you stay informed instead of relying on outdated information.

Are you making a big business decision?

Sometimes an appraisal has nothing to do with buying or selling. Maybe you’re bringing in a new business partner. Planning your estate. Appealing your property taxes. Handling a legal matter.

Or making long-term financial plans. When important decisions are involved, knowing your property’s value gives you confidence to move forward.

Maybe you’re just curious

And that’s perfectly okay. Not every property owner needs a special reason. Sometimes you simply want to know how your investment is doing. After all, you’ve worked hard for it. Knowing its current value helps you plan for the future with more confidence.

Conclusion:

If you’re asking yourself whether it’s time for a Commercial Property Appraisal, there’s a good chance it probably is. You don’t have to wait until someone tells you. You don’t have to wait until you’re under pressure.

Getting an appraisal now helps you understand where your property stands today.It gives you answers. It gives you confidence.

And it helps you make your next move knowing you’re working with real information—not guesses.

Frequently Asked Questions

When should I get a Commercial Property Appraisal?

If you’re thinking about selling, buying, refinancing, making upgrades, or just planning ahead — that’s a good time to get one. Knowing what your property’s worth before you make a big move? That gives you confidence to move forward.

Can I get an appraisal even if I’m not selling?

Yeah, absolutely. A lot of property owners just want to know where they stand. An appraisal gives you a clear picture of your investment, even if you got no plans to sell right now.

Why do banks ask for a Commercial Property Appraisal?

Banks wanna know what the property’s actually worth before they hand over a loan or approve a refinance. The appraisal gives them reliable info so they can make a smart decision.

Will renovations increase my property’s value?

They sure can. Things like a new roof, updated office space, parking lot repairs — those upgrades can bump up your value. An appraisal helps show exactly how those improvements affect what your property’s worth today.

How often should I update my appraisal?

If it’s been a few years or the local market’s changed, it’s a good idea to get an updated one. Property values don’t stay the same forever.

Is an online estimate enough?

An online estimate can give you a rough idea, but it doesn’t replace a professional appraisal. A real appraisal looks at your specific property and gives you a way more accurate number.

How long does the appraisal process take?

Most inspections take a few hours, depending on how big the property is. After that, the appraiser does their research and gets the final report ready within a few business days.

Can a Commercial Property Appraisal help with legal matters?

Yeah, for sure. Commercial appraisals are often used for estate planning, partnership changes, tax appeals, divorce cases.

Why choose 219 NWI Appraisal Group?

Because you get professional appraisal services backed by real local knowledge and years of experience serving Lake, Porter, and LaPorte Counties.

When someone applies for a commercial loan, the focus is usually on the business plan, credit profile, and financial strength. But there is another factor that carries just as much weight, sometimes even more.

The property itself.

Before a lender approves financing, they want a clear answer to one key question:

what is this commercial property actually worth in the current market

That is where a Commercial Appraisal comes in.

A Commercial Appraisal is a professional valuation that determines the market value of income-producing or business-related properties such as office buildings, retail spaces, warehouses, or mixed-use developments. It gives lenders an unbiased, data-backed understanding of the property’s true worth before they commit funds.

In simple speaking words, lenders are not just lending based on the borrower. They are also lending based on the property’s real value.

Why lenders cannot rely on purchase price alone

One common misunderstanding is that the purchase price of a property reflects its current value.

Lenders do not see it that way.

Prices can change due to:

market shifts

economic conditions

demand in the area

property condition changes

income potential fluctuations

Because of this, a Commercial Appraisal becomes necessary to confirm what the property is worth today, not what it was worth in the past.

How commercial appraisals reduce lending risk

From a lender’s perspective, every loan carries risk.

The property is usually the collateral, meaning it secures the loan if something goes wrong.

A Commercial Appraisal helps reduce that risk by showing:

fair market value

income-generating potential

comparable property performance

condition and usability

location strength

This allows lenders to make decisions based on real, measurable data instead of assumptions.

How lenders use the appraisal in approval decisions

A Commercial Appraisal is not just a formality. It directly influences how a loan is structured.

Lenders use it to determine:

how much they are willing to lend

loan-to-value ratio (LTV)

interest rate risk

repayment security

long-term investment stability

If the appraisal value is strong and well-supported, approval becomes smoother. If the value is lower than expected, lenders may adjust terms or reduce loan amounts.

What appraisers evaluate in commercial properties

Commercial properties are more complex than residential homes. That is why the appraisal process is more detailed.

An appraiser will typically review:

property size and layout

current condition

location and accessibility

rental income or occupancy rates

lease agreements (if applicable)

operating expenses

comparable commercial sales

All of this helps build a complete picture of the property’s financial performance and market position.

Income potential plays a major role

One of the biggest differences in a Commercial Appraisal is that value is often tied to income.

For income-producing properties, appraisers may look at:

rental income stability

tenant quality

lease length and terms

vacancy rates

operating costs

This is because lenders are not only interested in what the property is worth today, but also how it performs over time.

Why location is critical in commercial valuation

Just like residential real estate, location plays a major role, but in commercial properties, it can be even more important.

Lenders consider:

traffic flow and visibility

proximity to business hubs

accessibility for customers or logistics

surrounding commercial activity

future development plans

A strong location can significantly improve the outcome of a Commercial Appraisal, which in turn supports stronger lending decisions.

What happens if the appraisal value is lower than expected

This is a common situation in lending.

If the Commercial Appraisal comes in lower than anticipated:

loan amounts may be reduced

additional collateral may be required

interest terms may change

approval may be delayed or reconsidered

This is not meant to block financing. It is meant to align lending with real market conditions.

Why lenders trust independent appraisers

Lenders do not rely on internal opinions or borrower estimates.

They require independent professionals because:

it ensures neutrality

it removes bias

it follows regulated standards

it provides defensible documentation

it supports compliance requirements

That independence is what makes the Commercial Appraisal a trusted part of the lending process.

Conclusion:

Lenders require commercial appraisals because they need certainty in an uncertain market. They are not just approving people, they are also evaluating assets, risk, and long-term value.

A Commercial Appraisal brings clarity to that decision by showing what the property is truly worth based on real market data, income potential, and current conditions.

In the end, it helps both sides. Lenders reduce risk, and borrowers gain a clearer understanding of their property’s true financial position.

Frequently Asked Questions

What is a Commercial Appraisal?

It is a professional valuation of income-producing or business properties.

Why do lenders require it?

To understand the true market value of the property before approving a loan.

Does purchase price matter in lending decisions?

Not always, because market value may have changed since purchase.

What factors affect commercial property value?

Location, income potential, condition, and market demand all matter.

How does income affect valuation?

Rental income and occupancy rates can significantly influence value.

What is loan-to-value ratio?

It is the percentage of the loan compared to the appraised property value.

Can a low appraisal affect loan approval?

Yes, it may reduce loan amount or change lending terms.

Why is independent appraisal important?

It ensures unbiased and objective property valuation.

What properties need commercial appraisals?

Offices, retail buildings, warehouses, and mixed-use properties.

Why is it important for borrowers?

It helps them understand the true market value and financing limits of their property.

When a divorce happens, things rarely stay simple for long. What starts as a personal separation quickly turns into a financial discussion, and one of the biggest points of tension is usually the home.

Because the home is not just a building. It is a shared asset, a financial investment, and often the most valuable property involved.

And right at that moment, one question becomes unavoidable:

what is this property actually worth in today’s market

That is where a Divorce appraisal becomes necessary.

A Divorce appraisal is a professional, unbiased valuation that shows the fair market value of a property during a separation. It is not based on emotion, memory, or opinion. It is based on real market data and current conditions.

Courts rely on it because decisions about property division must be fair, and fairness only works when the value is accurate and neutral.

For families across Northwest Indiana, experienced professionals like 219NWI Appraisal Group provide these valuation services to help bring clarity during difficult and emotional situations.

Why courts do not accept guesswork in property value

In divorce cases, it is very common for each person to see the home differently.

One side may believe the value is higher because of improvements or personal attachment. The other side may believe it is lower due to repairs or market concerns.

But courts cannot work with two different opinions.

They need one clear, supportable value.

That is why a Divorce appraisal is used instead of:

online valuation tools

informal real estate opinions

emotional estimates

outdated purchase prices

These methods may give a general idea, but they do not provide the level of accuracy required for legal decisions.

How a Divorce appraisal brings balance into the situation

The most important role of a Divorce appraisal is to remove bias.

There is no negotiation inside the appraisal itself.

A professional appraiser does not take sides. There is no advantage in increasing or lowering the value for either party.

Instead, the focus stays completely on facts such as:

real market conditions

recent comparable home sales

property condition at the time of inspection

neighborhood trends

standard valuation methods

This creates a value that is balanced, neutral, and acceptable in court.

What courts expect from a proper Divorce appraisal

Courts do not just want a final number written on paper.

They want to understand how that number was reached.

A complete Divorce appraisal includes:

full property inspection

analysis of similar homes recently sold

explanation of differences and adjustments

review of current market trends

written justification of the final value

This level of detail makes the report strong enough to stand in a legal setting.

How property value directly affects divorce settlements

Once the home is valued correctly, everything else becomes easier to structure.

That value can influence:

buyout decisions

division of shared assets

equity distribution

financial settlement planning

If the value is too high or too low, the entire settlement can become unbalanced and unfair.

That is why courts depend on Divorce appraisals before finalizing property-related decisions.

Why market conditions cannot be ignored

Property value is never fixed. It changes with the market.

Appraisers carefully study:

supply and demand in the area

recent sales activity

interest rate changes

buyer behavior

neighborhood growth or decline

A Divorce appraisal reflects the real market at the time of valuation, not past assumptions or emotional expectations.

That is what makes it reliable for legal use.

Why local knowledge matters so much in Northwest Indiana

Even within the same region, property values can vary widely.

Across Lake, Porter, and LaPorte counties, value is influenced by:

school districts

neighborhood demand

employment access

nearby development

recent comparable sales

That is why courts rely on professionals like 219NWI Appraisal Group who understand local conditions and can reflect them accurately in the appraisal report.

How appraisers actually determine value

The process is structured and based entirely on evidence.

An appraiser will:

inspect the property in detail

evaluate condition and features

compare similar properties in the area

adjust for differences between homes

analyze current market trends

develop a final supported value

Every step is documented and based on real data, not assumptions.

That is what gives a Divorce appraisal its legal strength.

Why courts trust Divorce appraisals over other methods

Courts prefer Divorce appraisals because they are:

independent and unbiased

based on verified market data

professionally prepared

consistent with appraisal standards

defensible if challenged

This helps reduce disputes and gives both parties a fair starting point for resolution.

What happens without a proper appraisal

Without a Divorce appraisal, property value often becomes a source of conflict.

That can lead to:

ongoing disagreements

delays in settlement

emotional decision-making

repeated court discussions

Instead of clarity, there is confusion.

An appraisal helps prevent that by setting one agreed-upon value based on facts.

Conclusion:

Dividing property during divorce is never just about numbers. It is about fairness, clarity, and making sure both sides are treated equitably.

That is why courts rely on Divorce appraisals.

They remove emotion from the process and replace it with structured, evidence-based valuation that can be trusted in legal decisions.

With experienced support from 219NWI Appraisal Group, families across Northwest Indiana can move through this process with clearer understanding and more confidence in the outcome.

Frequently Asked Questions

What is a Divorce appraisal?

A professional valuation that determines the fair market value of a property during divorce.

Why do courts rely on Divorce appraisals?

Because they provide neutral and evidence-based property values.

Can emotional opinions be used instead?

No, courts require objective and data-supported valuations.

How does a Divorce appraisal help settlements?

It provides a fair value for asset division and buyout decisions.

Who performs Divorce appraisals?

Licensed appraisers with real estate market expertise.

What affects property value in divorce cases?

Condition, location, market trends, and comparable sales.

Can one appraisal be used for both parties?

Yes, courts often rely on a single neutral report.

Why is local market knowledge important?

Because property values vary significantly between neighborhoods.

What happens without an appraisal?

Disputes increase and settlements often get delayed.

Why is accuracy important in divorce valuation?

Because financial decisions depend on a fair and reliable property value.

When a property is involved in bankruptcy, everything becomes more sensitive, more time-bound, and much more dependent on accurate numbers. It is not just about what a home is worth in a normal situation. It is about what it is worth under pressure, under financial stress, and often under market conditions where a quick or forced sale may be likely.

That is where a Bankruptcy Appraisal comes in.

Professionals like 219NWI Appraisal play an important role in this process across Lake, Porter, and LaPorte counties by providing accurate and defensible distressed property valuations.

What is really happening in a Bankruptcy Appraisal

In a normal sale, a property is valued based on ideal market conditions.

But in bankruptcy, things are different.

The property may need to be sold quickly, or under pressure, or in a situation where the seller cannot wait for the best possible offer.

So a Bankruptcy Appraisal asks a different kind of question:

what would this property realistically sell for under distressed or forced conditions

That is the core idea.

The appraiser looks at:

current market conditions

comparable sales, including distressed sales

urgency of sale scenarios

property condition and repairs needed

buyer demand in similar situations

Then the value is adjusted to reflect reality, not ideal expectations.

Why Bankruptcy Appraisal is different from a normal appraisal

This is where many people get confused.

A standard residential appraisal assumes a normal market sale. There is time, negotiation, and typical buyer behavior.

A Bankruptcy Appraisal is different because:

time is often limited

seller may be under financial pressure

property may not be maintained properly

sale conditions may not be ideal

market exposure may be restricted

So the valuation must reflect those realities, not just textbook market value.

How appraisers actually handle distressed property valuations

This process is very structured, but also very realistic.

First, the appraiser evaluates the property’s current physical condition. In bankruptcy cases, properties may show signs of neglect or deferred maintenance, so condition matters a lot.

Then they study the local market, including both standard sales and distressed sales like:

foreclosures

short sales

auction sales

bank-owned properties

After that, they compare similar properties in similar conditions and similar urgency levels.

Then adjustments are made based on:

how quickly the property needs to sell

repair requirements

buyer demand under distressed conditions

neighborhood market stability

Finally, a Bankruptcy Appraisal report is prepared showing a realistic liquidation or market-adjusted value.

Why distressed property valuation matters in bankruptcy

This is the most important part of the entire process.

Bankruptcy cases are legal and financial situations where accuracy is critical.

A Bankruptcy Appraisal helps because:

courts need fair market or liquidation value

trustees need clarity on asset worth

creditors need accurate repayment estimates

legal decisions depend on documented values

disputes over asset value can be avoided

Without a proper appraisal, decisions may be based on assumptions instead of facts.

What makes distressed property harder to value

Distressed properties are not always straightforward.

Several factors can affect value, including:

lack of maintenance

urgent sale requirements

limited buyer interest

financial pressure on seller

neighborhood market conditions

Because of this, appraisers cannot rely only on standard sales data. They must also understand how distressed properties behave in the market.

How appraisers adjust value in bankruptcy cases

One of the key skills in a Bankruptcy Appraisal is making accurate adjustments.

Appraisers typically adjust for:

repair costs needed to bring the property to market condition

reduced buyer competition in distressed sales

time constraints affecting sale price

differences between normal and forced sales

risk factors affecting buyers

These adjustments help ensure the final value reflects real-world selling conditions.

Why accuracy is so important in bankruptcy situations

Even a small difference in valuation can have a big impact.

If a property is overvalued:

debt repayment calculations may be incorrect

legal disputes may arise

unrealistic expectations may delay proceedings

If a property is undervalued:

creditors may not receive fair repayment

asset distribution may become unfair

That is why accuracy in a Bankruptcy Appraisal is critical.

Professionals like 219NWI Appraisal ensure that valuations are based on real market behavior in Lake, Porter, and LaPorte counties.

What happens after the appraisal is completed

Once the Bankruptcy Appraisal report is prepared, it is used in:

court proceedings

trustee evaluations

creditor negotiations

asset liquidation planning

It becomes the official reference point for deciding how the property will be handled.

Conclusion:

A Bankruptcy Appraisal is a realistic reflection of what a property is worth under financial stress and real-world selling conditions.

It helps bring clarity in situations where timing, pressure, and legal requirements all come together.

In Lake, Porter, and LaPorte counties, experienced professionals like 219NWI Appraisal play an important role in making sure distressed property valuations are accurate, fair, and legally reliable.

Frequently Asked Questions

What is a Bankruptcy Appraisal?

It is a professional valuation that shows what a property is worth during financial distress or bankruptcy conditions.

How is it different from a normal appraisal?

It considers distressed market conditions, urgency of sale, and reduced buyer interest, unlike a normal market appraisal.

Why is it needed in bankruptcy?

It helps courts, trustees, and creditors understand the true value of assets for fair financial decisions.

What does distressed property mean?

It refers to properties sold under financial pressure, such as foreclosure, bankruptcy, or urgent liquidation.

How do appraisers determine value?

They use comparable sales, including distressed sales, property condition, and market demand under similar conditions.

Does condition affect value more in bankruptcy?

Yes, condition plays a major role because distressed properties often require repairs or urgent sale adjustments.

Can market value and bankruptcy value be different?

Yes, bankruptcy value is often lower due to urgency and distressed sale conditions.

Who uses Bankruptcy Appraisal reports?

Courts, trustees, lenders, attorneys, and sometimes creditors use these reports.

How long does it take?

Usually a few days to a couple of weeks depending on property complexity.

Why is professional appraisal important in bankruptcy?

Because legal and financial decisions require accurate, unbiased, and defensible property valuations.

A Date of Death Appraisals is one of those things most families only come to understand when they are already in the middle of probate and everything feels like paperwork, decisions, and emotional weight all at once. In that moment, there is usually very little clarity around property value, even though it becomes one of the most important parts of the entire estate process.

Not today’s value, not future value, but that specific point in time. That single number becomes the base for legal, tax, and inheritance decisions.

This is why professionals like 219NWI Appraisal working across Lake, Porter, and LaPorte counties are often involved, because they bring a clear, neutral, and market-based answer when families need it most.

What is really happening in a Date of Death Appraisals?

Think of it in a very real-life situation.

Someone passes away and leaves behind a home. Now the legal system needs to know one thing very clearly:

what was this home actually worth on the day they passed away

That is all a Date of Death Appraisals is trying to answer.

The appraiser looks at:

what similar homes were selling for around that exact time

what the market was doing on that date, not today

the actual condition of the property at that moment

how location and neighborhood value behaved at that time

Then everything is brought together into one clear and fair value based on that specific date.

Why does this matter so much in probate?

This is where people realize how important this step really is.

Probate is not just about transferring ownership. It is also about making sure everything is valued correctly so it can be divided or reported properly.

A Date of Death Appraisals helps because:

it gives a legally accepted value for the estate

it prevents confusion among family members

it helps avoid arguments over what the home is worth

it supports tax and court requirements

it keeps the process moving without delays

Without it, everyone may have a different idea of value, and that is where problems usually begin.

How probate issues usually start without a proper appraisal?

Most issues don’t start with conflict. They start with uncertainty.

Without a Date of Death Appraisals, families often rely on:

current market value instead of historical value

online estimates that don’t reflect timing

personal opinions about what the home “should” be worth

outdated or incomplete information

And because of that, every person involved may end up looking at a different number.

That is where confusion turns into disagreement.

Date of Death Appraisals actually works in real life

Even though it sounds technical, the process is very structured and practical.

First, the appraiser identifies the exact date of death and studies what the real estate market looked like at that time.

Then they find comparable homes that sold around that same period.

After that, they evaluate the property based on how it actually was on that date, not how it looks today.

Then they adjust for things like size, condition, location, and market behavior during that specific time.

Finally, everything is put into a clear report that shows the property’s value as of the date of death.

That report becomes the official reference used in probate and estate matters.

Why timing is everything in this process

One small detail can completely change the outcome, timing.

A property can change value over months depending on the market, so using today’s price would not be accurate for legal purposes.

A Date of Death Appraisals focuses only on:

the exact date the person passed away

the market conditions on that day

the real buyer behavior at that time

That precision is what makes it legally meaningful.

How it helps avoid family disputes

This is one of the biggest real-world benefits.

When there is no clear value, families may disagree because each person sees things differently.

A Date of Death Appraisals helps because:

everyone works from one agreed number

emotional opinions are removed from valuation

fairness becomes easier to see

discussions become more structured

Instead of debating value, the focus shifts to moving forward.

How it supports legal and tax requirements

In probate, numbers are not optional, they are required.

A Date of Death Appraisals supports this by:

providing a documented market value

meeting legal reporting requirements

supporting estate tax calculations

giving courts reliable valuation evidence

This is why it is often a required step, not just an optional one.

Why local knowledge matters in Lake, Porter, and LaPorte counties

Location plays a big role in accuracy.

Even nearby areas can have different pricing based on:

neighborhood demand

school districts

market activity

local development trends

That is why firms like 219NWI Appraisal are important, because they understand how values actually move in these specific counties and can produce more accurate, defensible reports.

What happens when Date of Death Appraisals is skipped

When this step is missed, things often become slower and more complicated.

It can lead to:

delays in probate processing

disagreements between heirs

incorrect estate reporting

confusion over property value

additional legal steps later

What should be a clear process becomes uncertain.

Conclusion:

A Date of Death Appraisals is not just a formality. It is what brings clarity when everything else feels uncertain.

It makes sure the property value is recorded fairly, based on the exact moment it matters legally.

In probate situations across Lake, Porter, and LaPorte counties, having an accurate and professionally prepared appraisal from experts like 219NWI Appraisal helps families avoid confusion and move through the process with more confidence and less conflict.

Frequently Asked Questions

What is a Date of Death Appraisals?

It is a professional valuation that shows what a property was worth on the exact date a person passed away.

Why is it needed in probate?

It is needed to provide a legal and accurate property value for estate settlement and tax purposes.

Does it use current market value?

No, it uses the market value from the exact date of death, not today’s value.

Who requests it?

Usually executors, attorneys, or family members handling the estate request it.

What happens without it?

Without it, probate can face delays, disputes, and confusion over property value.

How is the value calculated?

It is based on comparable sales, market conditions, and property details from that specific time period.

How long does it take?

It usually takes a few days to a couple of weeks depending on data and property details.

Why is local expertise important?

Because property values differ by area, local knowledge ensures accurate and reliable results.

Can family members disagree with it?

Yes, but a professional appraisal is generally accepted in legal and probate settings.

Is it required for every estate?

Not always, but it is strongly recommended and often required for accurate probate and tax reporting.

Estate settlement appraisal is something that usually comes into the picture at a very emotional time, when everything already feels a bit overwhelming. There is loss, there is paperwork, there are legal steps, and on top of that there is a property that now needs to be handled properly.

At that point, most people are not thinking about numbers or market data. They are thinking about family, memories, and fairness.

But the system still needs one clear thing.

A proper value.

And that is exactly what an estate settlement appraisal provides. It is just a professional way of answering one question clearly:

what is this property actually worth if we look at the real market, not emotions, not opinions, just facts

In places like Northwest Indiana, where property values can vary depending on the neighborhood, the timing, and the condition, this becomes even more important. That is why experienced professionals like 219NWI Appraisal Group are often involved to bring clarity and fairness into the process.

What is really happening in estate settlement appraisal

Think of it like this in a very real-world way.

When a property becomes part of an estate, everyone involved needs one shared understanding of value. Without that, every conversation turns into different opinions, and that is where confusion starts.

So an estate settlement appraisal is basically doing one thing:

removing guesswork and replacing it with a clear market-based number

The appraiser is not deciding what the house should be worth emotionally. They are simply looking at what the market would realistically pay for it.

They check:

what similar homes sold for recently

what condition the property is in

how strong the neighborhood demand is

what the market was doing at that time

Then all of that gets turned into one fair value.

Why estate settlement appraisal becomes so important

This is where things become very practical.

Because once a property is part of an estate, it is no longer just a home. It becomes a financial asset that needs to be handled properly.

And this is where an estate settlement appraisal helps in a big way.

It is used for:

dividing property fairly among heirs

legal probate requirements

calculating estate taxes correctly

deciding whether to sell or keep the property

preventing misunderstandings between family members

Without it, everything is based on opinions, and opinions can easily lead to disagreement.

With it, there is a clear reference point everyone can look at.

How estate settlement appraisal actually works?

Even though it sounds technical, the process is actually very logical.

First, the appraiser looks at the property as it is right now. No assumptions, just reality.

Then they go back and look at similar homes that were sold in the same area during the relevant time.

After that, they study the market conditions like demand, pricing behavior, and how active buyers were.

Then they adjust for differences like size, layout, condition, and upgrades.

And finally, everything comes together into a final estate settlement appraisal value.

It is structured, step by step, and based on real data.

What executors need to understand clearly

Executors often carry the responsibility of moving everything forward, and that can feel like a lot.

So one thing is very important to understand:

an estate settlement appraisal is not something to influence or shape based on emotion

It is something to support with correct information.

Executors should focus on:

giving full access to the property

sharing accurate documents

avoiding delays in the process

staying neutral and organized

Their role is to keep things moving properly, not to adjust the outcome.

What heirs usually realize during the process

Heirs often come in expecting a certain value or hoping for a certain outcome, which is completely natural.

But over time, one thing becomes clear:

the estate settlement appraisal is based only on market reality, not personal expectations

That means:

memories do not increase value

emotional attachment does not change price

opinions are not part of the calculation

Once that is understood, the process becomes easier to accept, even if the number is different from what was expected.

Common mistakes that create confusion

A lot of problems in estate situations do not come from the appraisal itself, but from misunderstandings around it.

Some common mistakes include:

thinking emotional value affects pricing

assuming renovations automatically increase estate value

using estimates instead of proper reports

delaying the appraisal too long

not sharing complete property details

These small things can slow everything down or create unnecessary tension.

Why professionals matter so much here

An estate settlement appraisal is often used in legal and tax situations, so it cannot be casual or approximate.

It needs to be:

neutral

well-documented

based on real market data

acceptable for court or tax use

That is why firms like 219NWI Appraisal Group are trusted in Northwest Indiana. They understand both the technical side and the sensitivity of estate situations.

The easiest way to think about an estate settlement appraisal is like taking a financial snapshot of a property at a specific moment in time.

Not what it could become Not what someone hopes it should be Just what it realistically is worth based on the market

That snapshot becomes the foundation for everything else that follows.

Conclusion:

An estate settlement appraisal is not just about numbers on a page. It is about bringing clarity into a situation that is often emotional and complex.

When done properly, it helps families move forward with fairness, reduces conflict, and ensures everything is handled based on real market value instead of confusion or assumptions.

Frequently Asked Questions

What is an estate settlement appraisal?

An estate settlement appraisal is a professional way of finding out what a property is worth after someone passes away, based on real market conditions rather than opinions or emotions.

Why is estate settlement appraisal needed?

It is needed so property can be divided fairly, taxes can be calculated correctly, and legal requirements during estate settlement can be properly completed.

Who is responsible for ordering the appraisal?

Usually the executor of the estate, probate attorneys, or family members handling legal settlement are responsible for ordering it.

Does emotional value affect estate settlement appraisal?

No, emotional value does not affect the appraisal at all. Only market data and property condition are used.

How is the value calculated in estate settlement appraisal?

It is calculated using recent comparable sales, property condition, location, and market trends from the relevant time period.

How long does the process usually take?

It usually takes a few days to a couple of weeks depending on property complexity and available market data.

What happens after the appraisal is completed?

The final value is used for probate court, tax reporting, inheritance distribution, or deciding whether to sell the property.

Why is local knowledge important in estate settlement appraisal?

Because property values vary by area, especially in regions like Northwest Indiana, local market understanding helps ensure accurate valuation.

Can heirs disagree with the appraisal?

They can question it if there is strong evidence of error, but professional appraisals are generally accepted in legal processes.

What is the biggest mistake people make?

The biggest mistake is assuming emotional value or expectations affect price instead of understanding that estate settlement appraisal is based only on real market data.

When someone thinks about investing in property, the first thing that usually comes to mind is the price.But experienced investors don’t start with the asking price. They start with a question that matters more.

What is this property actually worth in the real market right now?

And that is exactly where an investment appraisal becomes important. Because property value is not something guessed or assumed. It is something built step by step using real data, real comparisons, and real market conditions.

Why property value is never just a simple number

A property may look valuable on the surface. Clean building, good location, decent structure.

But in an investment appraisal, value is never based on appearance alone.

Two properties can look almost the same and still have completely different values.

Why?

Because value is shaped by real-world conditions like demand, location strength, condition, and income potential.

That is why professionals never rely on assumptions.

They rely on structured valuation.

So how is property value actually decided in an investment appraisal?

Let’s break it down in a simple, real way.

An investment appraisal looks at different factors together to reach a fair and realistic value.

1. What are similar properties selling for right now?

This is usually the first check.

Instead of guessing, the appraiser looks at real sales in the same area.

So the question becomes:

What did similar properties actually sell for recently?

If similar homes are selling higher, value goes up. If they are selling lower, value adjusts down.

Simple, but very powerful.

2. Where exactly is the property located?

Location is one of the biggest drivers of value.

And the question here is very direct:

Is this location in demand or not?

An investment appraisal checks things like:

Is the area growing or declining?

Are people moving in or out?

How strong is the neighborhood demand?

What facilities are nearby?

Even small location differences can change value significantly.

3. What condition is the property in?

This is where reality really matters.

So the question becomes:

Is the property move-in ready or does it need work?

An appraiser looks at:

Age of the structure

Maintenance level

Repairs needed

Renovations already done

A well-maintained property always holds stronger value in an investment appraisal.

4. Can this property generate income?

For investment properties, this question matters a lot:

How much money can this property actually make?

An investment appraisal looks at:

Rental income potential

Tenant demand in the area

Occupancy stability

Long-term cash flow

If income potential is strong, value usually increases.

5. What is happening in the overall market?

Property value is never isolated.

So another important question is:

Is the market currently strong or weak?

An investment appraisal studies:

Demand vs supply

Buyer activity

Price trends

Economic conditions

When demand is high and supply is low, value rises. When supply increases, value stabilizes or drops.

6. Is the area going to grow in the future?

Smart investors don’t only look at today.

They also ask:

What will this area look like in a few years?

An investment appraisal considers:

New infrastructure projects

Road or transport development

Commercial expansion

Population growth

Future growth potential can significantly increase present value.

How the full investment appraisal process actually happens

Property valuation is not done randomly. It follows a clear process.

First step: What is the property like in reality?

The appraiser checks structure, condition, and features in detail.

Second step: What is happening in the market?

Recent sales, trends, and demand levels are studied.

Third step: How does it compare?

Similar properties are used as real benchmarks.

Final step: What is the fair value?

All findings come together into one clear investment appraisal report.

Why investors don’t skip this step anymore

Because guessing is expensive.

An investment appraisal helps investors avoid:

Overpaying for a property

Buying in weak locations

Underestimating repair costs

Missing hidden risks

Making emotional decisions

It turns uncertainty into clarity.

And clarity is what protects money.

What changes when appraisal is done first?

Everything becomes more controlled.

Instead of asking:

Is this a good deal?

Investors start asking:

Does the value actually support this deal?

That shift alone changes how decisions are made.

Negotiations become stronger. Risks become visible. Choices become clearer.

That is the real advantage of an investment appraisal.

Conclusion:

Property investment is not just about finding something that looks good. It is about understanding what it is truly worth in today’s market. An investment appraisal brings all the important factors together—market trends, condition, location, and future potential—into one clear valuation.

When that value is known, decisions stop being emotional and start becoming strategic.

And in investing, that difference matters more than anything else.

Frequently Asked Questions

What does an investment appraisal really mean in property?

It means checking the real market value of a property using data, comparisons, and market conditions before making an investment decision.

What is the first thing checked in valuation?

Usually, recent sales of similar properties in the same area are checked first.

Why is location such a big factor?

Because demand, growth, and future value depend heavily on where the property is located.

Does property condition affect value?

Yes, condition plays a major role in increasing or reducing value in an investment appraisal.

How does rental income affect value?

Higher and stable rental income usually increases overall property value.

Why is market trend important?

Because value changes based on demand, supply, and overall market activity.

Can future development increase value?

Yes, upcoming infrastructure and growth plans can raise property value over time.

Why do investors prefer appraisal before buying?

To avoid overpaying and to understand real risk before committing money.

What happens if appraisal is skipped?

It can lead to wrong pricing, poor returns, and unexpected losses.

Who performs investment appraisals?

Trained property appraisers or valuation professionals with market experience.

Real estate appraisals is what really sets the tone in any property decision, because before anything moves forward in buying, selling, refinancing, or even legal settlement, someone has to clearly say what the property is actually worth in today’s market. Not what the owner feels it is worth, not what the buyer hopes it is worth, but what the market genuinely supports.

And that is exactly where real estate appraisals come in. It is a structured, professional way of putting a real number on a property using facts, comparisons, and market behavior.

Call Us Now (847) 521-9584 219NWI Appraisal Group

Let’s make real estate appraisals

Real estate appraisals are basically a professional way of saying, here is what this property is worth right now.

No guessing. No emotional value. No random online estimate.

What actually happens is simple: A trained appraiser looks at the property, studies the area, checks recent sales, and then builds a clear value report. That final number becomes the real estate appraisals result.

And that result is what banks, buyers, sellers, and courts trust.

Why real estate appraisals matters more than people think

Here’s something important to understand. Real estate appraisals are not just a formality. It actually protects money.

Because in real estate, even a small mistake in pricing can lead to big losses.

So real estate appraisals is used to:

Stop buyers from overpaying

Stop sellers from underpricing

Help banks approve safe loans

Support legal property settlements

Keep tax values accurate

So in simple words, real estate appraisals keeps everything fair and balanced.

Types of real estate appraisals explained

Now let’s go through the main types of real estate appraisals in a very practical way, the way it actually works in real situations.

Residential real estate appraisals

This is the one most people deal with.

Whenever someone is buying or selling a home, residential real estate appraisals comes into play.

It looks at:

The condition of the house

The layout and space

The neighborhood quality

Nearby recent home sales

So instead of guessing a price, residential real estate appraisals gives a grounded value based on real market activity.

Commercial real estate appraisals

Now when it comes to shops, offices, or business buildings, things work differently.

Commercial real estate appraisals is not just about structure, it is about income.

It focuses on:

Rental income potential

Business activity in the area

Demand for commercial space

Long term earning ability

So here, real estate appraisals is basically asking one question: how much money can this property generate?

Industrial real estate appraisals

Factories, warehouses, and production units fall here.

This type of real estate appraisals checks:

Land usability

Transport access

Industrial demand in the region

Operational value of the space

It is very practical and business focused, because these properties are used for production and logistics.

Divorce real estate appraisals

This is where things become sensitive.

During divorce, real estate appraisals makes sure property division is fair and based on facts, not emotions.

It helps to:

Decide fair property value

Split assets equally

Avoid disputes

Support legal decisions

So instead of arguments, real estate appraisals brings clarity.

Estate and inheritance real estate appraisals

When property is passed down, real estate appraisals is used to make sure everything is handled properly.

It helps in:

Dividing property among heirs

Setting tax values

Legal documentation

Avoiding family conflicts

This type of real estate appraisals is especially important because emotions are involved, but the value still needs to stay objective.

Tax appeal real estate appraisals

Sometimes property taxes feel too high compared to actual value.

This is where real estate appraisals is used to challenge that.

It helps:

Show true market value

Reduce tax burden

Support appeal cases

Correct overvaluation

So real estate appraisals becomes a tool for financial protection.

How real estate appraisals actually happens step by step

Let’s break it down in a way that feels real and easy to follow.

First step is property inspection

The appraiser physically checks the property. Not just looks at it, but studies it properly.

Then comes market comparison

Recent similar properties are checked. This is where real pricing reality comes in.

Then data is studied

Market trends, neighborhood changes, demand shifts all are reviewed.

Final step is report creation

Everything is put together into a clear valuation report.

That is how real estate appraisals is completed from start to finish.

Things that directly affect real estate appraisals value

Now let’s talk about what actually changes the number.

Location is always the strongest factor

Better location means stronger real estate appraisals value.

Condition of the property matters a lot

Well maintained homes always get better valuation.

Market demand changes everything

High demand areas push values up quickly.

Size and usability of space

Not just size, but how usable the space is matters more.

Legal clarity of property

Clean documents always support stronger real estate appraisals results.

Common mistakes people make with real estate appraisals

Here’s where people often go wrong.

Thinking renovation guarantees higher value

Relying only on online estimates

Comparing wrong properties

Ignoring market changes

Assuming emotional value matters

But real estate appraisals does not work on assumptions. It works on data.

Why real estate appraisals protects financial decisions

Think of real estate appraisals as a safety filter before big money moves.

It makes sure:

Buyers don’t overpay

Sellers don’t lose value

Banks don’t take risky loans

Legal cases stay fair

Taxes stay accurate

So every real estate appraisal result protects someone from making a costly mistake.

Quick comparison of real estate appraisals types

Type

What it focuses on

Residential

Home value and condition

Commercial

Income and business use

Industrial

Operational and land use

Divorce

Fair asset division

Estate

Inheritance value

Tax appeal

Correct tax valuation

Each real estate appraisal type serves a different situation but follows the same core logic.

Why professional real estate appraisals is always better

There is a big difference between guessing and professional evaluation.

Professional real estate appraisals gives:

Data backed value

Neutral judgment

Market accuracy

Legal acceptance

Financial safety

That is why banks, courts, and serious buyers always rely on it.

Role of 219NWI Appraisal Group

219NWI Appraisal Group provides structured and reliable real estate appraisal services designed to bring clarity in property decisions.

Their work focuses on:

Accurate valuation based on real market data

Detailed property inspection

Transparent reporting

Fast and reliable turnaround

Call Us Now (847) 521-9584

Conclusion:

At the end of the day, real estate appraisals is what keeps the property world stable. It removes confusion, reduces risk, and gives everyone a clear number to work with.

Whether it is a home, a commercial building, or a legal case, real estate appraisals is what turns uncertainty into clarity.

Frequently Asked Questions

Why is real estate appraisals important before making any property decision?

Real estate appraisals is important because it provides a clear and unbiased property value based on real market data, helping avoid financial mistakes in buying, selling, or lending situations.

How does real estate appraisals actually determine the final value of a property?

Real estate appraisals determines value by inspecting the property, comparing recent sales, and analyzing market trends to arrive at a fair and accurate market-based valuation.

What is the difference between residential and commercial real estate appraisals?

Residential real estate appraisals focus on home value and condition, while commercial real estate appraisals focuses on income potential and business use of the property.

Can real estate appraisals value change over time?

Yes, real estate appraisals value can change based on market conditions, neighborhood development, property improvements, and overall demand in the real estate market.

Why do banks require real estate appraisals before approving loans?

Banks use real estate appraisals to confirm that the property value supports the loan amount, reducing financial risk and ensuring secure lending decisions.

Does renovation always increase real estate appraisals value?

Not always. Some renovations increase value more than others, and real estate appraisals focuses on market impact rather than just renovation cost.

What happens if real estate appraisals value is lower than expected?

If real estate appraisals comes lower, buyers may renegotiate price, or sellers may adjust expectations based on actual market conditions.

How long does a typical real estate appraisals process take?

Most real estate appraisals processes take a few days depending on property size, inspection time, and data analysis requirements.

Why is location so important in real estate appraisals?

Location affects demand, accessibility, and neighborhood value, making it one of the strongest factors in real estate appraisals results.

Who performs real estate appraisals in professional settings?

Certified appraisers perform real estate appraisals using structured methods, market data, and inspection processes to ensure accurate and unbiased valuation.

Real Estate Appraisal is the process used to figure out what a property is really worth in the open market, especially when people are arguing about it. Courts rely on Real Estate Appraisal because it keeps things fair, simple, and based on facts instead of opinions. When there is a dispute in divorce, inheritance, taxes, or business separation, this is what usually brings clarity.

It is basically the number everyone agrees to follow when emotions and disagreements make things messy.

Why Real Estate Appraisal is used in court cases

Real Estate Appraisal is used because courts don’t want guesses or emotional claims. They want a clear, neutral value that can stand in front of both sides.

Here’s why it matters

It keeps decisions fair for both parties

It removes personal bias and emotions

It shows the real market value

It gives judges something solid to rely on

So instead of arguing “what I think it’s worth,” the court looks at “what the market proves.”

How courts actually use Real Estate Appraisal

Real Estate Appraisal becomes evidence in court. Judges don’t just glance at it, they study it carefully before making a decision.

What usually happens

The appraisal report is submitted as proof

Both sides review and question it

Experts may explain how the value was calculated

Courts compare multiple appraisals if needed

If one side disagrees, the court may bring in another independent Real Estate Appraisal to balance things out.

How Real Estate Appraisal is done step by step

Real Estate Appraisal follows a proper process so the final number is not random.

The process usually looks like this

The property is inspected properly

The local market is studied

Similar properties are compared

Condition, size, and location are checked

A final value is prepared and reported

Methods commonly used

Sales comparison method (most common)

Cost method (what it costs to rebuild)

Income method (if it earns rent)

Each method supports the final Real Estate Appraisal value in its own way.

What changes the value in Real Estate Appraisal

Real Estate Appraisal is not fixed. It changes based on real conditions in the market and property.

Key factors that matter

Where the property is located

How the property looks and its condition

What similar homes recently sold for

Current demand in the area

Legal limits like zoning rules

Even a small upgrade or damage can change the Real Estate Appraisal value.

Why accuracy in Real Estate Appraisal is so important

Real Estate Appraisal needs to be very accurate because courts make decisions based on it. If the number is wrong, the outcome can be unfair.

Why courts care about accuracy

It affects money division directly

It prevents unfair advantage

It reduces legal fights later

It builds trust in the decision

A strong Real Estate Appraisal can decide how smoothly a case ends.

Common mistakes in Real Estate Appraisal

Real Estate Appraisal can go wrong if the process is rushed or incomplete.

Common problems

Using outdated property data

Comparing the wrong properties

Ignoring repairs or damage

Not understanding the local market

When mistakes happen, the Real Estate Appraisal can be challenged in court.

How lawyers use Real Estate Appraisal

Real Estate Appraisal is a big support tool for lawyers during disputes.

How it helps in cases

Helps negotiate fair settlements

Used as evidence in hearings

Helps challenge the other side’s claims

Guides clients on what to expect

It becomes the “proof point” in most property arguments.

Real situations where Real Estate Appraisal is used

Real Estate Appraisal shows up in many everyday legal disputes.

Common examples

Divorce where property is split

Family inheritance disagreements

Business partners separating assets

Tax value disagreements with authorities

In all these cases, Real Estate Appraisal helps bring a final number everyone can work with.

Best way to get a strong Real Estate Appraisal

A strong Real Estate Appraisal comes from proper work, not shortcuts.

What makes it reliable

Experienced certified appraiser

Fresh market research

Full property inspection

Honest property comparisons

When these are followed, the Real Estate Appraisal stands strong even in court.

Conclusion:

Real Estate Appraisal is basically the anchor in property disputes. When people argue and emotions run high, it brings everything back to facts. Courts depend on it because it keeps decisions fair and grounded in real market value. Without Real Estate Appraisal, cases would turn into opinions. With it, there is structure, clarity, and fairness.

Frequently Asked Questions

What exactly is Real Estate Appraisal used for in court?

Real Estate Appraisal is used in court to figure out the fair market value of a property so judges can make fair decisions in disputes like divorce, inheritance, taxes, or business separation cases.

Why do judges trust Real Estate Appraisal reports?

Judges trust Real Estate Appraisal because it is based on real market data, property comparisons, and professional methods instead of personal opinions or emotional claims from either side.

Can someone disagree with a Real Estate Appraisal?

Yes, a Real Estate Appraisal can be challenged if one party feels it is incorrect. Courts may then review it or order another independent appraisal to compare values.

Who prepares Real Estate Appraisal for legal cases?

Real Estate Appraisal is prepared by certified and licensed appraisers who are trained to evaluate property value using standard methods and real market data.

What makes Real Estate Appraisal go up or down?

Location, property condition, market demand, and recent sales of similar homes all affect Real Estate Appraisal value and can increase or decrease it depending on changes.

How long does Real Estate Appraisal usually take?

Real Estate Appraisal usually takes a few days to a couple of weeks depending on how complex the property is and how much data needs to be collected and analyzed.

What happens if two Real Estate Appraisal reports are different?

If two Real Estate Appraisal reports don’t match, the court compares both and may request a third independent opinion to reach a fair final value.

Is Real Estate Appraisal important in divorce cases?

Yes, Real Estate Appraisal is very important in divorce cases because it helps divide property fairly based on real market value instead of assumptions or emotional claims.

What information is needed for Real Estate Appraisal?

Property records, ownership documents, tax details, and information about repairs or upgrades are usually needed to complete a proper Real Estate Appraisal.

Why is Real Estate Appraisal so important in disputes?

Real Estate Appraisal is important because it removes guesswork, reduces conflict, and gives courts a clear and fair value to make legal decisions.